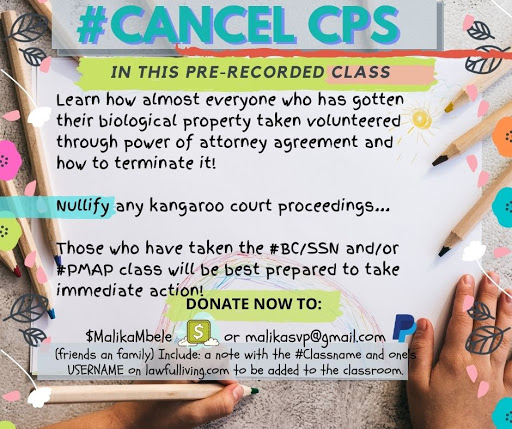

Woman Beat CPS DHHS without going to court!

Click the image below to join our private membership community to take this class

⭐ALERT! Supreme & Lower Courts Rule “No License Necessary to Drive on Public Highways”

I’m NOT a lawyer and nothing in this video is to be taken as legal advice. This is simply a reading of a lower court and Supreme Court cases regarding…

Meeting The Deputy For The First Time

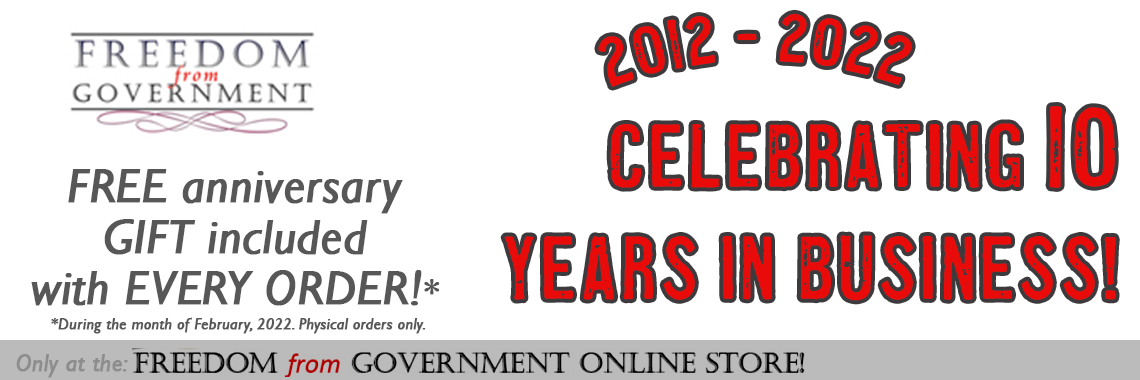

Celebrating our 10 YEAR ANNIVERSARY!

Everyone gets 5 free stickers but we are also giving away 3 dash cams, 10 .999 fine American silver eagles, free aluminum signs, books and MORE! Just place an order…

Insurance is a scam.

There was a time when you didn’t have to buy car insurance. Risky? Reckless? Maybe. But one thing’s certain: All of us now have to spend exorbitant sums on insurance…

Objection!

This is a list of objections in American law: Proper reasons for objecting to a question asked of a witness include:Ambiguous, confusing, misleading, vague, unintelligible: the question is not clear…

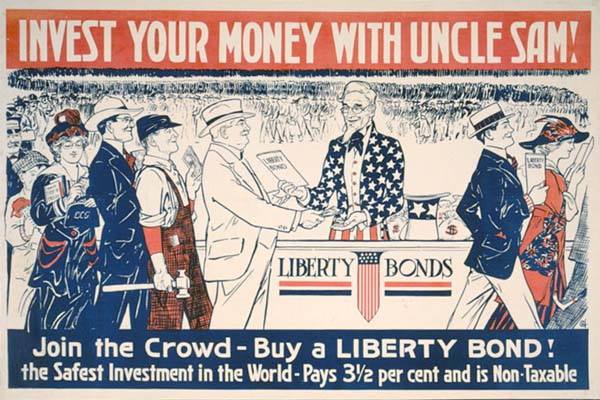

From War Bonds to Prison Bonds

When you go in the courts they always say they are operating under a statute jurisdiction. The Black’s Law Dictionary 4th edition says a statute is a bond or obligation…

The old empire is the new empire.

The Roman Empire used licenses to establish sovereign authority over her conquered subjects. Rome generously declared that her subjects could worship any god they chose and in any manner they…

Beat Any Victimless Case in America

I am constantly getting the question: “I got arrested and now I have court in a week… what do I do???†Right away I want to say that the following…